M&A presentations always look remarkably clean in PowerPoint. There are synergy targets, strategic fit discussions, and value creation plans, usually illustrated by a few overlapping circles that suggest everyone will seamlessly integrate and harmonise bank accounts by Friday afternoon.

Then treasury gets involved.

The reality is often far less straightforward. Questions quickly emerge about who actually owns which bank accounts, cash forecasting disappears into layers of inherited spreadsheets, payment processes stop working as expected, guarantees remain attached to the wrong entities, and treasury is asked a few weeks before go-live whether setting up a new cash pool will be a simple exercise.

Unfortunately, it rarely is. Humanity somehow managed to build nuclear submarines before learning how to migrate bank signatories efficiently.

What makes M&A, carve-outs, and demergers particularly challenging for treasury is that the function sits at the centre of so many critical processes. Treasury touches cash, banking relationships, liquidity management, payments, FX exposure, debt facilities, guarantees, systems, controls, legal entities and business continuity. When treasury is involved early, many risks can be anticipated and managed. When it is overlooked, the consequences tend to surface later, often at the most inconvenient and expensive moment.

For treasurers navigating the beautiful chaos of corporate transactions, here are 10 practical tips that can make the journey a little smoother.

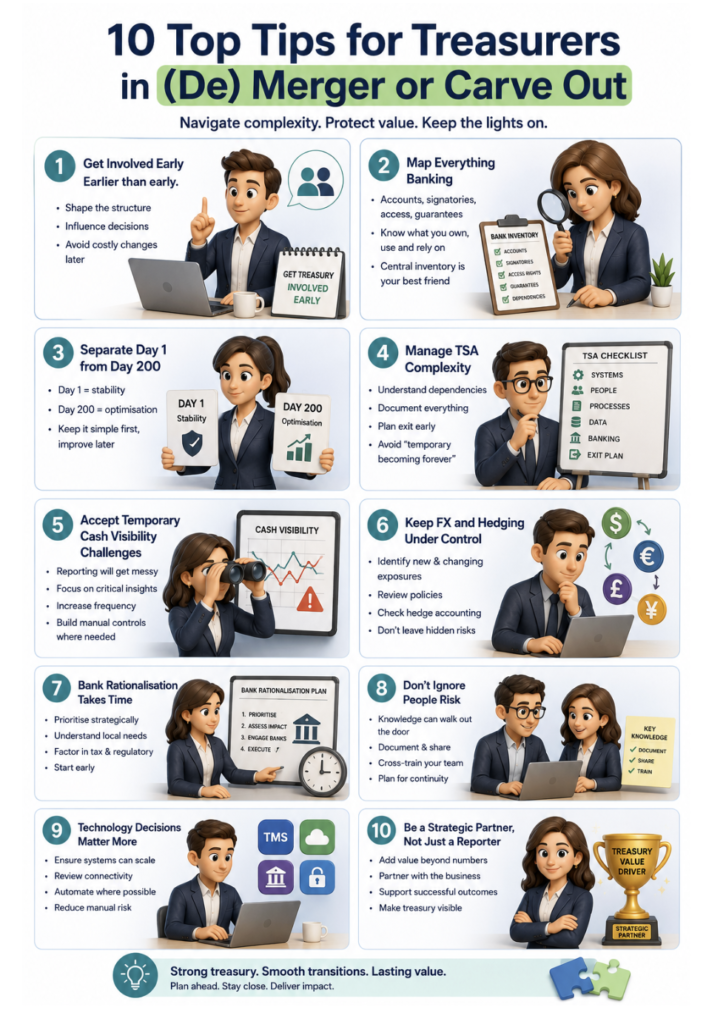

1. Get Treasury Involved Early. Earlier Than Early.

One of the most common mistakes in M&A projects is involving treasury only after the major strategic decisions have already been made. By that stage, legal structures may have been designed without considering banking arrangements, payment flows, financing structures, FX exposures, or liquidity management requirements.

What looks logical from a corporate or legal perspective can create significant challenges for treasury. Cash pools may no longer function as intended because entities move across jurisdictions or ownership structures change. Intercompany funding arrangements may need to be redesigned, existing guarantees and letters of credit reviewed, and banking relationships reassessed.

Treasury should therefore be involved during the planning phase, not just during execution. Early input can help shape decisions around bank account structures, liquidity management, intercompany funding, guarantees, debt facilities, FX exposures, payment continuity, and the impact on ERP and treasury management systems.

When treasury joins the project late, the result is often a more complex, expensive, and highly manual implementation process. Consultants tend not to mind this phase, of course. Someone has to run all those emergency workshops.

2. Map Every Bank Account and Signatory

At first glance, this sounds like one of the most straightforward tasks in an M&A project. In reality, many organisations discover during mergers, demergers, and carve-outs that they do not have a fully reliable overview of:

- Bank accounts

- Signatories

- E-banking users

- Payment approval rights

- Guarantees

- Local banking arrangements

- Dormant accounts

Corporate transactions have a remarkable ability to expose operational gaps that have accumulated over the years. Information that is assumed to exist often turns out to be incomplete, outdated, or spread across multiple teams and systems.

To avoid surprises later in the process, create a central inventory as early as possible and document:

- Who owns the account?

- Which entity uses it?

- What systems connect to it?

- Which payment flows run through it?

- Who can approve payments?

- Are there dependencies with cash pools or netting structures?

It may not be the most exciting part of the project, but it is one of the most important. A well-maintained banking inventory can prevent countless delays, risks, and last-minute discoveries when the transaction reaches critical milestones.

3. Separate Day 1 From Day 200

One of the most common traps during an M&A project is trying to design the perfect future-state treasury organisation from the outset. While the long-term vision is important, focusing on optimisation too early can distract from what matters most: ensuring the business can operate successfully on Day 1.

Before discussing ideal structures, advanced automation, or future treasury enhancements, make sure the fundamentals are covered:

- Can employees get paid?

- Can suppliers get paid?

- Can customers still pay you?

- Are bank statements arriving?

- Does liquidity visibility exist?

- Can treasury still control risk?

The first priority should always be operational continuity. Once the transaction has been completed and the organisation is functioning independently, there will be time to improve processes, redesign structures, and optimise the treasury model.

Day 1 is about stability and keeping the business running. Day 200 is where optimisation begins. Organisations that confuse those two objectives often find themselves facing avoidable project delays, unnecessary complexity, and increasingly nervous CFOs.

4. Don’t Underestimate TSA Complexity

Transition Service Agreements (TSAs) often sound straightforward on paper. In practice, they usually exist because separating systems, processes, and responsibilities is far more complicated than the deal timeline allows. What appears to be a temporary arrangement is often the result of years of interconnected operations that cannot be untangled overnight.

From a treasury perspective, TSAs can cover a wide range of critical activities, including:

- Shared bank connectivity

- Shared TMS environments

- Shared ERP payment factories

- Shared guarantees

- Shared FX hedging programmes

- Shared in-house banks

- Shared netting structures

While these arrangements can provide essential continuity after a transaction closes, they also create dependencies that need to be actively managed. Responsibilities, service levels, costs, and decision-making authority should be clearly documented from the outset.

Most importantly, every TSA should have a well-defined exit plan. Without clear ownership and realistic timelines for separation, temporary solutions have a tendency to outlive their original purpose and become semi-permanent fixtures of the organisation. Few things are more enduring than a “temporary” process that nobody prioritised replacing.

5. Expect Cash Visibility to Get Worse Before It Gets Better

One reality of almost every merger, integration, demerger, or carve-out is that cash visibility tends to deteriorate before it improves. As entities move, bank connectivity changes, reporting lines are redesigned, and data ownership shifts between teams, the quality of forecasting and reporting often suffers. Information that was previously available through established processes suddenly becomes harder to access or less reliable.

Accepting this early is important. Trying to maintain the same level of reporting accuracy and forecasting precision during a period of significant structural change can create unrealistic expectations and unnecessary frustration.

The priority during this phase should not be reporting perfection but maintaining control over liquidity and ensuring critical decisions can still be made with confidence. Many treasury teams find themselves increasing reporting frequency, focusing on key cash positions, and introducing temporary controls to compensate for gaps in systems or data flows.

Treasury professionals generally dislike manual processes, and for good reason. However, during an M&A project, a temporary spreadsheet, reconciliation, or manual control can sometimes provide more value than waiting months for the perfect automated solution. The goal is to keep the business running safely through the transition, not to win awards for process design.

6. FX and Hedging Can Get Messy Fast

Many treasury teams assume they have a good understanding of their FX risk profile until a merger, acquisition, or carve-out forces them to look again. Transactions often introduce new currencies, new intercompany flows, different supply chain structures, and even changes to functional currencies. Exposures that previously did not exist can emerge surprisingly quickly, while existing hedging programmes may no longer align with the organisation’s new structure.

Early in the process, treasury should assess which exposures will disappear, which new risks will emerge, and what the transaction means for existing hedge accounting relationships and financing facilities. Particular attention should be paid to carve-outs, where standalone entities often inherit FX risks that were previously managed centrally.

Because nothing says “successful integration” quite like discovering several million euros of unmanaged FX exposure halfway through the first quarter close.

7. Bank Rationalisation Takes Longer Than Expected

Almost every M&A presentation promises efficiencies through bank rationalisation. Almost every treasury team discovers that achieving those efficiencies is far more complicated than expected.

What initially appears to be a simple exercise quickly runs into local banking dependencies, regulatory requirements, tax considerations, ERP limitations, lengthy onboarding processes, and KYC reviews that seem to require documentation dating back several decades.

Closing bank accounts across multiple jurisdictions can take months and, in some cases, years. The most effective approach is usually to start early, focus first on strategically important countries, and build realistic timelines into the project plan. Experience suggests that every major KYC process will eventually require at least one document that nobody can locate anymore.

8. Don’t Ignore People Risk

When organisations assess M&A risks, they often focus on systems, structures, and processes. What is sometimes overlooked is that a significant amount of treasury knowledge exists only in the heads of a small number of people.

During integrations and carve-outs, roles change, responsibilities shift, workloads increase, and key employees occasionally leave. At the same time, treasury is expected to maintain full control over liquidity, payments, risk management, and banking operations.

Protecting institutional knowledge should therefore be a priority from the start. Critical processes need to be documented, key banking relationships recorded, system access mapped, and sufficient backups established for approvals and operational activities. Cross-training team members may not feel urgent when the project begins, but it often becomes invaluable later.

Treasury teams are usually smaller than senior management assumes. Sometimes considerably smaller.

9. Technology Decisions Matter More Than Ever

M&A projects have a remarkable ability to expose weaknesses in treasury infrastructure. Systems that function adequately during normal operations can struggle when entities are added, removed, or reorganised within a short timeframe.

Questions around treasury technology should therefore be addressed early. Can the TMS accommodate significant organisational changes? Can bank connectivity scale quickly enough? Are payment workflows flexible? Can the ERP structure support the future operating model? And perhaps most importantly, how much of the current reporting process still relies on manually maintained spreadsheets?

This is often where specialised treasury support becomes particularly valuable. Not because internal treasury teams lack expertise, but because they are simultaneously responsible for running daily operations while helping redesign the operating model around them.

Redesigning the aircraft while keeping it in the air remains one of humanity’s more ambitious hobbies.

10. Treasury Should Not Be an Afterthought

The most successful M&A projects recognise treasury as a strategic workstream rather than an operational support function. Treasury sits at the centre of cash management, funding, risk management, payments, banking, systems, controls, and operational continuity. Few functions have such a broad impact across the organisation.

When treasury encounters problems during a merger or carve-out, the consequences are felt quickly throughout the business. Payments fail, liquidity visibility deteriorates, controls weaken, and financial risks become harder to manage. Conversely, when treasury is involved early, supported appropriately, and given sufficient resources, integrations tend to progress more smoothly and with fewer surprises.

Not painlessly, of course. It is still M&A.

Final Thought

Mergers, demergers, and carve-outs are rarely just finance projects. More often, they are large-scale operational separation and integration exercises disguised as strategic initiatives.

Throughout the process, treasury is frequently the function quietly holding everything together while the rest of the organisation focuses on synergy targets, transaction announcements, and integration plans. The irony is that treasury usually attracts attention only when something goes wrong: payments stop, liquidity becomes uncertain, controls fail, or unexpected FX losses appear.

Which is precisely why treasury deserves a seat at the table from the very beginning.

At Pecunia Treasury & Finance, we support organisations through complex treasury challenges associated with mergers, acquisitions, carve-outs, and transformations. This can involve interim treasury expertise, treasury transformation support, TMS implementation and optimisation, bank connectivity projects, cash management, FX risk management, or simply providing additional capacity when internal teams are stretched.

Sometimes, the most valuable contribution is helping treasury teams focus on the transaction itself by temporarily taking operational pressure off their shoulders.

Because during M&A, having people involved who understand treasury beyond a list of keywords turns out to be surprisingly useful.

A surprisingly high bar in modern recruitment, apparently.